What exactly is VIX?

The market’s expectations for the relative strength of impending price swings of the S&P 500 Index are reflected in the Cboe Volatility Index (VIX), a live index (SPX). It produces a 30-day forecast of volatility drawn from the pricing of SPX index options with close-in expiration dates. 1 Volatility, or how quickly prices fluctuate, is frequently used to assess market emotion, particularly the level of anxiety among traders.

The index frequently refers to as “the VIX” despite being known by its ticker symbol. Managed by Cboe Global Markets and developed by the Cboe Options Exchange (Cboe). Because it offers a measurable gauge of market risk and investor emotion. It is a crucial index in the world of crypto currency trading platform and investing.

What Is the VIX’s Process?

The S&P 500’s price swings attempted to be gauged using the VIX (i.e., its volatility). The level of volatility rises in direct proportion to how dramatically the index’s price swings change and vice versa. In addition to using VIX as a volatility index. Traders can also use it to bet on changes in volatility by trading VIX futures, options, and ETFs.

Generally speaking, there are two ways to calculate volatility. The first approach uses statistical calculations on prior prices over a given time period and is based on historical volatility. On the historical pricing data sets, numerous statistical quantities such as mean (average), variance, and standard deviation were calculated.

The VIX employs the second method, which entails estimating its value based on implied option prices. 1 Options are derivative financial products, and the price of an option depends on the likelihood that the price of a particular stock will increase by a specific amount (called the strike price or exercise price).

The volatility factor, which is an integral input parameter for many option pricing models (including the Black-Scholes model), represents the likelihood that such price changes will occur within the specified time frame.

Since option prices are found on the open market used to calculate the underlying security’s volatility. This volatility refers as forward-looking implied volatility when implied by or inferred from market prices (IV).

The VIX’s Method of Measuring Market Volatility

The cryptocurrency market participants’ upbeat attitude is demonstrated by the level of fewer than 20 points. Despite the calm and optimism, this frequently denotes a trend reversal, necessitating the closing of positions with riskier instruments. 20 to 30 is a typical range that does not show any appreciable changes.

The market is in a frenzy if the level rises by at least 40 points. During this time, the value of stocks, emerging market currencies, and commodity assets typically collapse over the world.

However, these declines were seen as the ideal opportunity to invest in hazardous assets. After all, their worth will start to increase once the situation is fixed. Therefore, the CBOE Volatility Index research aids the investor in determining the best entry and exit points for their trades as well as how the trend is growing and when to correct their positions.

The asset’s historical volatility displays price movements over a specific time period. A trader can forecast the future price range by analyzing implied volatility (also known as future volatility). Be aware that VIX also aids traders in estimating the potential changes in correlated indicators like SPX.

How to Determine the VIX

Based on the premiums that investors are ready to pay for the ability to buy or sell an option on the S&P 500 Index, the Volatility Index value is a broad assumption. The weighted average of all option prices in the S&P 500 Index is hence the VIX.

The S&P 500 Index’s projected movement over the following 30 calendar days is roughly represented by the VIX values, which are expressed as percentages and recalculated annually. Therefore, if the VIX number is 15, the predicted annual change is 15%.

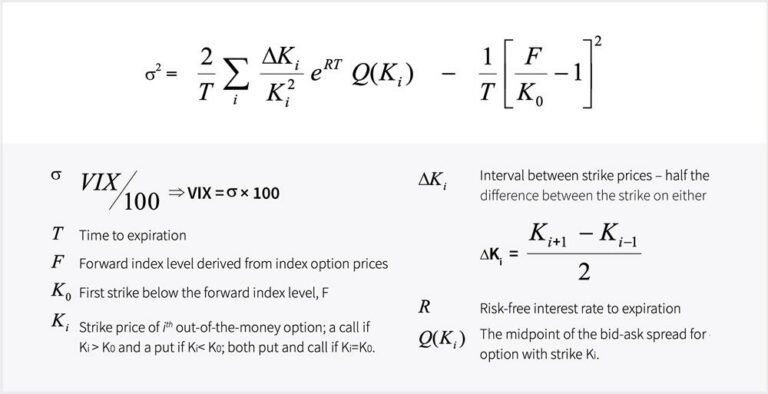

The full Formula for Calculating the VIX Index Appears to be Somewhat Challenging

The square root of the value of the crypto exchange India rate movement for the subsequent 30 days, beginning today, is used to compute VIX. Keep in mind that the VIX measures swap change volatility, not swap volatility (volatility that is the square root of the change or standard deviation). Swap volatility requires dynamic hedging, whereas swap change may be entirely statically replicated using just put and call. The risk-neutral estimate of variations in the S&P 500 over the upcoming 30 calendar days is represented by the square root of the VIX. The annualized standard deviation used in the VIX quote.

Options having a maturity of 23 to 27 days are considered in the calculation. One hundred is added to the VIX volatility value. For instance, if the VIX is 20, there will be 20% volatility.

The favored volatility index used by the media, replacing the earlier VXO, is now the VIX. VXO was a gauge of implied volatility derived from S&P 100 Index 30-day options.

The VIX index is an essential tool in every trader’s toolbox. Investors can use it to monitor asset price performance and determine its current trend. Additionally, VIX correlates with other indicators and aids analysts in predicting the movement of those indicators (which can be the opposite of VIX). Even though the calculation is challenging, you don’t have to do it by hand because most trading platforms enable and display the volatility index.

Visit us at: www.bitcoiva.com